- 0

- 타이쿤

- 조회 수 88

https://www.martinsosnoff.com/post/my-inner-game-of-investing

My Inner Game Of Investing

- Martin Sosnoff

- Nov 6, 2023

- 3 min read

I am for better or worse mainly a contrary investor. Whenever I’m within the consensus I’d worry that I can’t possibly outperform the Averages. Today, I’m no more than 35% long equities, the cross I carry is a burden.

Whenever the market has a zippy day I trail. I do own Microsoft and Amazon but little else in tech. Heavy in energy with Occidental Petroleum and Enterprise Products Partners. On a zippy day for tech houses my oils can turn negative.

I don’t own GDP stocks like GM, GE, and Deere. For me, many tech houses are overpriced and under-analyzed. I dig Microsoft’s financial reporting as fairly complete, and understandable, so I own it. Likewise, Amazon, where I am happily overweighted, too.

Mid-sixties, after Boeing ramped up its 707 jet, airlines turned into growth stocks. Money brokers then financed my convertible debentures on 10% margin. I cashed in Eastern Airlines at $400, and Boeing, United Aircraft, and United Airlines convertibles all hit double par for me. I had enough capital to start my own money management firm and haven’t worked for anyone since I’m 30.

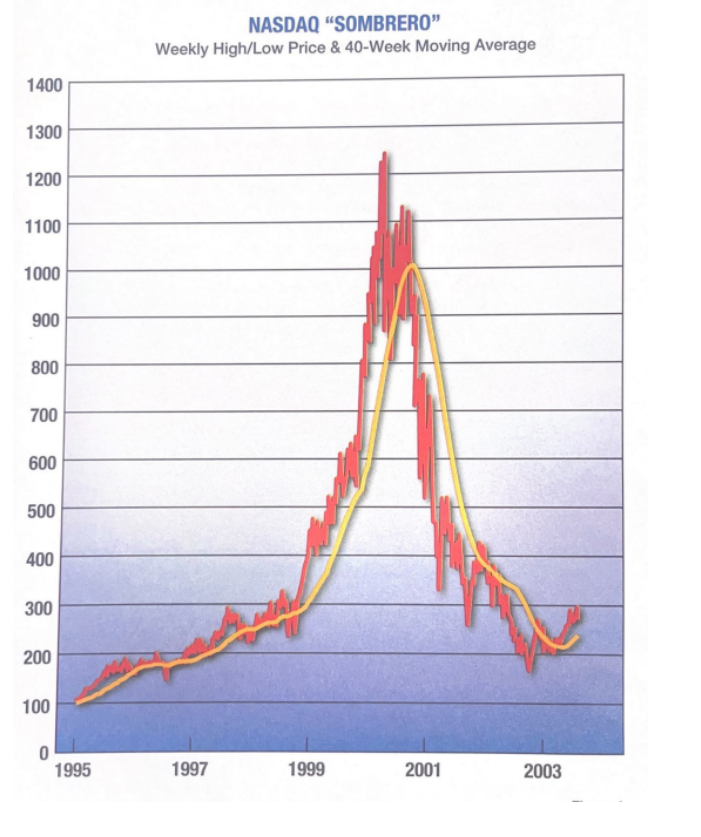

The stock options market early seventies embraced a coterie of market makers with minimal capital. Manny had graduated from OTC trading desks. They understood and could calculate volatility. Perhaps, not so precisely as the Black Scholes model that decades later, garnered a Nobel Prize in economics, but well enough to get by and not muff price quotes on puts and calls. I wasn’t smart enough to short NASDAQ at its peak, in 2000. The late Leon Levy, an old friend, shorted NASDAQ, and went long on the euro, one of the few simple but great spreads that rode the peak of the NASDAQ sombrero down to its right side’s wide brim. If you have to think about a great concept, even a short, for more than 15 minutes, it’s probably not a good idea.

My ‘73–’74 caper in the options market delivered comparable percentage gains to Leon’s, but on a much smaller scale. Leon logged nine-figure money. It took just one phone call to his Bear Stearns trader. I had to hondle with a bunch of Market dealers.

My number one trader at Solomon Brothers, Symphony Sid, sheparded, my options orders through the Chicago Board of Trade. The “Roids” stood for Polaroid and the “Cabuie” for the Chicago Options Exchange. Sid was Symphony Sid because of his running patter on trades, minute by minute. Can you imagine?

As for FRB policy initiatives today, I don’t see any tightening that will clamp down on the market’s price-earnings ratio. So I carry huge positions in 2 and 10-year Treasuries. Unwinding of the negative yield curve to 20 basis point feeds my inner voice and tells me to buy 10-year paper yielding over 5%.

Problem is I never carried a big bond portfolio, underleveraged in Treasuries, either long or short. Easier to carry overweighted positions in Amazon and Microsoft. Analysts have struck out on their earnings calls for most tech houses. This never changes.

If you believe the 10-year Treasury yield is headed for 7%, dig yourself a fox hole and jump in for the duration. The price-earnings ratio for the market could wilt to no more than 15 times earnings. This is another way of saying, biggest risk today is the confidence level for stock and bonds. Too much tension wherever you look.

내 투자 심리

마틴 소스노프

2023년 11월 6일

읽기 3분

좋든 나쁘든 저는 주로 반대 투자자입니다. 시장 컨센서스 범위 안에 있을 때는 평균 수익률을 상회할 수 있을지 걱정합니다. 현재 저는 주식 매수 비중을 35% 이하로 유지하고 있는데, 제가 보유한 교차 매수 포지션은 부담스럽습니다.

시장이 활황일 때는 저는 뒤처집니다. 저는 마이크로소프트와 아마존을 보유하고 있지만, 다른 기술주는 거의 보유하고 있지 않습니다. 옥시덴탈 페트롤리엄과 엔터프라이즈 프로덕츠 파트너스의 에너지주에 주로 투자합니다. 기술주가 활황일 때는 원유 가격이 마이너스로 떨어질 수 있습니다.

저는 GM, GE, 디어와 같은 GDP 관련 주식은 보유하고 있지 않습니다. 저에게 많은 기술주들이 고평가되어 있고 분석이 부족합니다. 저는 마이크로소프트의 재무 보고서가 상당히 완벽하고 이해하기 쉽다고 생각해서 보유하고 있습니다. 아마존도 마찬가지로, 저는 아마존에 대해서도 기꺼이 비중을 확대하고 있습니다.

1960년대 중반, 보잉이 707 제트기 생산을 늘리면서 항공사들은 성장주로 전환했습니다. 그 후 금융 중개인들이 제 전환사채를 10%의 증거금으로 조달해 주었습니다. 이스턴 항공을 400달러에 현금화했고, 보잉, 유나이티드 항공, 유나이티드 항공의 전환사채는 모두 제게 두 배의 수익을 안겨주었습니다. 저는 자금 관리 회사를 설립할 만큼 충분한 자본을 확보했고, 30세 이후로는 아무에게도 일한 적이 없습니다.

1970년대 초 주식 옵션 시장은 자본이 거의 없는 시장 조성자 집단을 포용했습니다. 매니는 장외 거래 데스크를 졸업했습니다. 그들은 변동성을 이해하고 계산할 수 있었습니다. 수십 년 후 노벨 경제학상을 수상한 블랙 숄즈 모델만큼 정확하지는 않았지만, 풋옵션과 콜옵션의 가격 변동을 무시하지 않고 버틸 만큼은 충분했습니다. 2000년, 나스닥이 정점에 달했을 때 저는 공매도 포지션을 취할 만큼 현명하지 못했습니다. 오랜 친구였던 고(故) 레온 레비는 나스닥을 공매도하고 유로화를 매수했습니다. 유로화는 나스닥 솜브레로의 정점을 오른편의 넓은 가장자리까지 끌어내린 몇 안 되는 간단하지만 훌륭한 스프레드 중 하나였습니다. 훌륭한 아이디어, 심지어 공매도 전략에 대해 15분 이상 고민해야 한다면, 그건 좋은 생각이 아닐 것입니다.

1973년에서 1974년 사이에 제가 옵션 시장에서 벌인 투자는 레온의 투자 수익률과 비슷한 수준의 수익을 가져왔지만, 그 규모는 훨씬 작았습니다. 레온은 9자리 수의 수익을 올렸습니다. 베어스턴스 트레이더에게 전화 한 통이면 충분했습니다. 저는 여러 명의 마켓 딜러들과 씨름해야 했습니다.

솔로몬 브라더스에서 제 주전 트레이더였던 심포니 시드가 시카고 상품거래소(CBOT)를 통해 제 옵션 주문을 처리해 주었습니다. "로이드(Roids)"는 폴라로이드(Polaroid)를, "카부이(Cabuie)"는 시카고 옵션 거래소(Chicago Options Exchange)를 뜻합니다. 시드는 매 순간 매매를 반복했기 때문에 심포니 시드였습니다. 상상이 되시나요?

오늘 FRB 정책 이니셔티브에 대해 말씀드리자면, 시장의 주가수익비율(PER)을 억제할 만한 긴축 조치는 보이지 않습니다. 그래서 저는 2년물과 10년물 국채에 막대한 포지션을 보유하고 있습니다. 마이너스 수익률 곡선이 20bp까지 풀리면서 제 내면의 목소리가 들려와 5% 이상의 수익률을 내는 10년물 국채를 사라고 재촉합니다.

문제는 제가 국채에 롱 포지션이든 숏 포지션이든 레버리지를 낮춘 대규모 채권 포트폴리오를 보유해 본 적이 없다는 것입니다. 아마존과 마이크로소프트에 대한 비중 확대 포지션을 보유하는 것이 더 쉽습니다. 애널리스트들은 대부분의 기술주에 대한 실적 발표를 취소했습니다. 이는 결코 변하지 않습니다.

10년물 국채 수익률이 7%로 향하고 있다고 생각하신다면, 과감하게 투자 기간을 늘려보세요. 시장의 주가수익비율(PER)은 15배를 넘지 않을 수도 있습니다. 즉, 오늘날 가장 큰 위험은 주식과 채권에 대한 신뢰 수준이라는 뜻입니다. 어디를 보더라도 긴장감이 너무 높습니다.